Česky

ČeskyData Harvesting – Extract, Transform, Load

It is important to have a rich and comprehensive data set for every system decision, including machine learning models. Only then can one build a robust and powerful model with desired performance. Otherwise, the developer would face the so-called GIGO (garbage in – garbage out) effect. It is an expression…

It is important to have a rich and comprehensive data set for every system decision, including machine learning models. Only then can one build a robust and powerful model with desired performance. Otherwise, the developer would face the so-called GIGO (garbage in – garbage out) effect. It is an expression…Complexity of each calculation in the StockPicking Lab

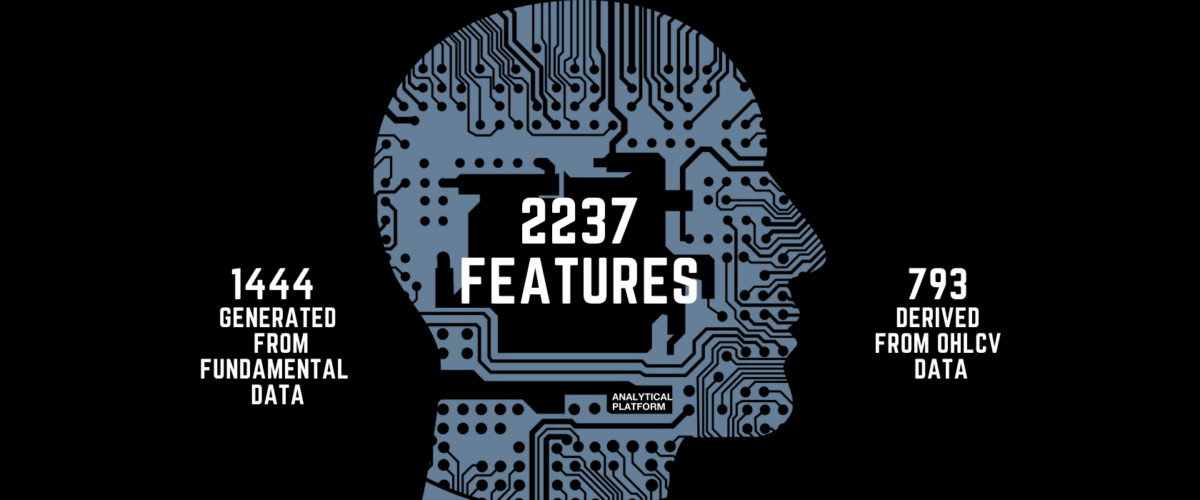

The use of machine learning in the quantitative investment field is expanding and the right usage is encouraging many to explore the world of investing. To generate market advantages and enable our users to enjoy the greatest stock selection process, we are choosing beneficial data, suitable to give us not…

The use of machine learning in the quantitative investment field is expanding and the right usage is encouraging many to explore the world of investing. To generate market advantages and enable our users to enjoy the greatest stock selection process, we are choosing beneficial data, suitable to give us not…New SFA features

We have deployed a new version of our SFA (Summary of Financial Articles) software. We have recently added: filtering articles according to the date of their publication, from one day to an unlimited long history. determining sentiment either directly in the articles about selected tickers or in all articles where…

We have deployed a new version of our SFA (Summary of Financial Articles) software. We have recently added: filtering articles according to the date of their publication, from one day to an unlimited long history. determining sentiment either directly in the articles about selected tickers or in all articles where…Model Diagnostics with Learning Curves

Reviewing learning curves of models during training and plots of the measured performance can be used to diagnose problems with learning, such as an underfitting or overfitting model. Besides that, it can also be used for diagnosing whether the training and validation datasets are suitably representative and to observe generalization…

Reviewing learning curves of models during training and plots of the measured performance can be used to diagnose problems with learning, such as an underfitting or overfitting model. Besides that, it can also be used for diagnosing whether the training and validation datasets are suitably representative and to observe generalization…Feature Selection

As part of the research used, for example, in the StockPicker application we have been researching the selection of variables enterings. When there are too many variables, the model has a worse ability to generalize and therefore is less robust and more prone to errors. If you need to extract…

As part of the research used, for example, in the StockPicker application we have been researching the selection of variables enterings. When there are too many variables, the model has a worse ability to generalize and therefore is less robust and more prone to errors. If you need to extract…Feature Binning and Quantile Transformation

As part of the research used, for example, in the StockPicker application, we have recently implemented the method Feature Binning and Quantile Transformation to better classify data. Due to upgraded data preparation, our machine learning models now achieve better results. You can see this in detail in the following lines.…

As part of the research used, for example, in the StockPicker application, we have recently implemented the method Feature Binning and Quantile Transformation to better classify data. Due to upgraded data preparation, our machine learning models now achieve better results. You can see this in detail in the following lines.…